9. Production Smoothing via Inventories#

Contents

In addition to what’s in Anaconda, this lecture employs the following library:

!pip install quantecon

Show code cell output

Requirement already satisfied: quantecon in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (0.7.2)

Requirement already satisfied: numba>=0.49.0 in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from quantecon) (0.59.0)

Requirement already satisfied: numpy>=1.17.0 in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from quantecon) (1.26.4)

Requirement already satisfied: requests in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from quantecon) (2.31.0)

Requirement already satisfied: scipy>=1.5.0 in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from quantecon) (1.11.4)

Requirement already satisfied: sympy in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from quantecon) (1.12)

Requirement already satisfied: llvmlite<0.43,>=0.42.0dev0 in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from numba>=0.49.0->quantecon) (0.42.0)

Requirement already satisfied: charset-normalizer<4,>=2 in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from requests->quantecon) (2.0.4)

Requirement already satisfied: idna<4,>=2.5 in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from requests->quantecon) (3.4)

Requirement already satisfied: urllib3<3,>=1.21.1 in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from requests->quantecon) (2.0.7)

Requirement already satisfied: certifi>=2017.4.17 in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from requests->quantecon) (2024.2.2)

Requirement already satisfied: mpmath>=0.19 in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from sympy->quantecon) (1.3.0)

9.1. Overview#

This lecture can be viewed as an application of this quantecon lecture about linear quadratic control theory.

It formulates a discounted dynamic program for a firm that chooses a production schedule to balance

minimizing costs of production across time, against

keeping costs of holding inventories low

In the tradition of a classic book by Holt, Modigliani, Muth, and Simon [Holt et al., 1960], we simplify the firm’s problem by formulating it as a linear quadratic discounted dynamic programming problem of the type studied in this quantecon lecture.

Because its costs of production are increasing and quadratic in production, the firm holds inventories as a buffer stock in order to smooth production across time, provided that holding inventories is not too costly.

But the firm also wants to make its sales out of existing inventories, a preference that we represent by a cost that is quadratic in the difference between sales in a period and the firm’s beginning of period inventories.

We compute examples designed to indicate how the firm optimally smooths production while keeping inventories close to sales.

To introduce components of the model, let

\(S_t\) be sales at time \(t\)

\(Q_t\) be production at time \(t\)

\(I_t\) be inventories at the beginning of time \(t\)

\(\beta \in (0,1)\) be a discount factor

\(c(Q_t) = c_1 Q_t + c_2 Q_t^2\), be a cost of production function, where \(c_1>0, c_2>0\), be an inventory cost function

\(d(I_t, S_t) = d_1 I_t + d_2 (S_t - I_t)^2\), where \(d_1>0, d_2 >0\), be a cost-of-holding-inventories function, consisting of two components:

a cost \(d_1 I_t\) of carrying inventories, and

a cost \(d_2 (S_t - I_t)^2\) of having inventories deviate from sales

\(p_t = a_0 - a_1 S_t + v_t\) be an inverse demand function for a firm’s product, where \(a_0>0, a_1 >0\) and \(v_t\) is a demand shock at time \(t\)

\(\pi\_t = p_t S_t - c(Q_t) - d(I_t, S_t)\) be the firm’s profits at time \(t\)

\(\sum_{t=0}^\infty \beta^t \pi_t\) be the present value of the firm’s profits at time \(0\)

\(I_{t+1} = I_t + Q_t - S_t\) be the law of motion of inventories

\(z_{t+1} = A_{22} z_t + C_2 \epsilon_{t+1}\) be a law of motion for an exogenous state vector \(z_t\) that contains time \(t\) information useful for predicting the demand shock \(v_t\)

\(v_t = G z_t\) link the demand shock to the information set \(z_t\)

the constant \(1\) be the first component of \(z_t\)

To map our problem into a linear-quadratic discounted dynamic programming problem (also known as an optimal linear regulator), we define the state vector at time \(t\) as

and the control vector as

The law of motion for the state vector \(x_t\) is evidently

or

(At this point, we ask that you please forgive us for using \(Q_t\) to be the firm’s production at time \(t\), while below we use \(Q\) as the matrix in the quadratic form \(u_t' Q u_t\) that appears in the firm’s one-period profit function)

We can express the firm’s profit as a function of states and controls as

To form the matrices \(R, Q, N\) in an LQ dynamic programming problem, we note that the firm’s profits at time \(t\) function can be expressed

where \(S_{c}=\left[1,0\right]\).

Remark on notation: The notation for cross product term in the QuantEcon library is \(N\).

The firms’ optimum decision rule takes the form

and the evolution of the state under the optimal decision rule is

The firm chooses a decision rule for \(u_t\) that maximizes

subject to a given \(x_0\).

This is a stochastic discounted LQ dynamic program.

Here is code for computing an optimal decision rule and for analyzing its consequences.

import matplotlib.pyplot as plt

plt.rcParams["figure.figsize"] = (11, 5) #set default figure size

import numpy as np

import quantecon as qe

class SmoothingExample:

"""

Class for constructing, solving, and plotting results for

inventories and sales smoothing problem.

"""

def __init__(self,

β=0.96, # Discount factor

c1=1, # Cost-of-production

c2=1,

d1=1, # Cost-of-holding inventories

d2=1,

a0=10, # Inverse demand function

a1=1,

A22=[[1, 0], # z process

[1, 0.9]],

C2=[[0], [1]],

G=[0, 1]):

self.β = β

self.c1, self.c2 = c1, c2

self.d1, self.d2 = d1, d2

self.a0, self.a1 = a0, a1

self.A22 = np.atleast_2d(A22)

self.C2 = np.atleast_2d(C2)

self.G = np.atleast_2d(G)

# Dimensions

k, j = self.C2.shape # Dimensions for randomness part

n = k + 1 # Number of states

m = 2 # Number of controls

Sc = np.zeros(k)

Sc[0] = 1

# Construct matrices of transition law

A = np.zeros((n, n))

A[0, 0] = 1

A[1:, 1:] = self.A22

B = np.zeros((n, m))

B[0, :] = 1, -1

C = np.zeros((n, j))

C[1:, :] = self.C2

self.A, self.B, self.C = A, B, C

# Construct matrices of one period profit function

R = np.zeros((n, n))

R[0, 0] = d2

R[1:, 0] = d1 / 2 * Sc

R[0, 1:] = d1 / 2 * Sc

Q = np.zeros((m, m))

Q[0, 0] = c2

Q[1, 1] = a1 + d2

N = np.zeros((m, n))

N[1, 0] = - d2

N[0, 1:] = c1 / 2 * Sc

N[1, 1:] = - a0 / 2 * Sc - self.G / 2

self.R, self.Q, self.N = R, Q, N

# Construct LQ instance

self.LQ = qe.LQ(Q, R, A, B, C, N, beta=β)

self.LQ.stationary_values()

def simulate(self, x0, T=100):

c1, c2 = self.c1, self.c2

d1, d2 = self.d1, self.d2

a0, a1 = self.a0, self.a1

G = self.G

x_path, u_path, w_path = self.LQ.compute_sequence(x0, ts_length=T)

I_path = x_path[0, :-1]

z_path = x_path[1:, :-1]

𝜈_path = (G @ z_path)[0, :]

Q_path = u_path[0, :]

S_path = u_path[1, :]

revenue = (a0 - a1 * S_path + 𝜈_path) * S_path

cost_production = c1 * Q_path + c2 * Q_path ** 2

cost_inventories = d1 * I_path + d2 * (S_path - I_path) ** 2

Q_no_inventory = (a0 + 𝜈_path - c1) / (2 * (a1 + c2))

Q_hardwired = (a0 + 𝜈_path - c1) / (2 * (a1 + c2 + d2))

fig, ax = plt.subplots(2, 2, figsize=(15, 10))

ax[0, 0].plot(range(T), I_path, label="inventories")

ax[0, 0].plot(range(T), S_path, label="sales")

ax[0, 0].plot(range(T), Q_path, label="production")

ax[0, 0].legend(loc=1)

ax[0, 0].set_title("inventories, sales, and production")

ax[0, 1].plot(range(T), (Q_path - S_path), color='b')

ax[0, 1].set_ylabel("change in inventories", color='b')

span = max(abs(Q_path - S_path))

ax[0, 1].set_ylim(0-span*1.1, 0+span*1.1)

ax[0, 1].set_title("demand shock and change in inventories")

ax1_ = ax[0, 1].twinx()

ax1_.plot(range(T), 𝜈_path, color='r')

ax1_.set_ylabel("demand shock", color='r')

span = max(abs(𝜈_path))

ax1_.set_ylim(0-span*1.1, 0+span*1.1)

ax1_.plot([0, T], [0, 0], '--', color='k')

ax[1, 0].plot(range(T), revenue, label="revenue")

ax[1, 0].plot(range(T), cost_production, label="cost_production")

ax[1, 0].plot(range(T), cost_inventories, label="cost_inventories")

ax[1, 0].legend(loc=1)

ax[1, 0].set_title("profits decomposition")

ax[1, 1].plot(range(T), Q_path, label="production")

ax[1, 1].plot(range(T), Q_hardwired, label='production when $I_t$ \

forced to be zero')

ax[1, 1].plot(range(T), Q_no_inventory, label='production when \

inventories not useful')

ax[1, 1].legend(loc=1)

ax[1, 1].set_title('three production concepts')

plt.show()

Notice that the above code sets parameters at the following default values

discount factor \(\beta=0.96\),

inverse demand function: \(a0=10, a1=1\)

cost of production \(c1=1, c2=1\)

costs of holding inventories \(d1=1, d2=1\)

In the examples below, we alter some or all of these parameter values.

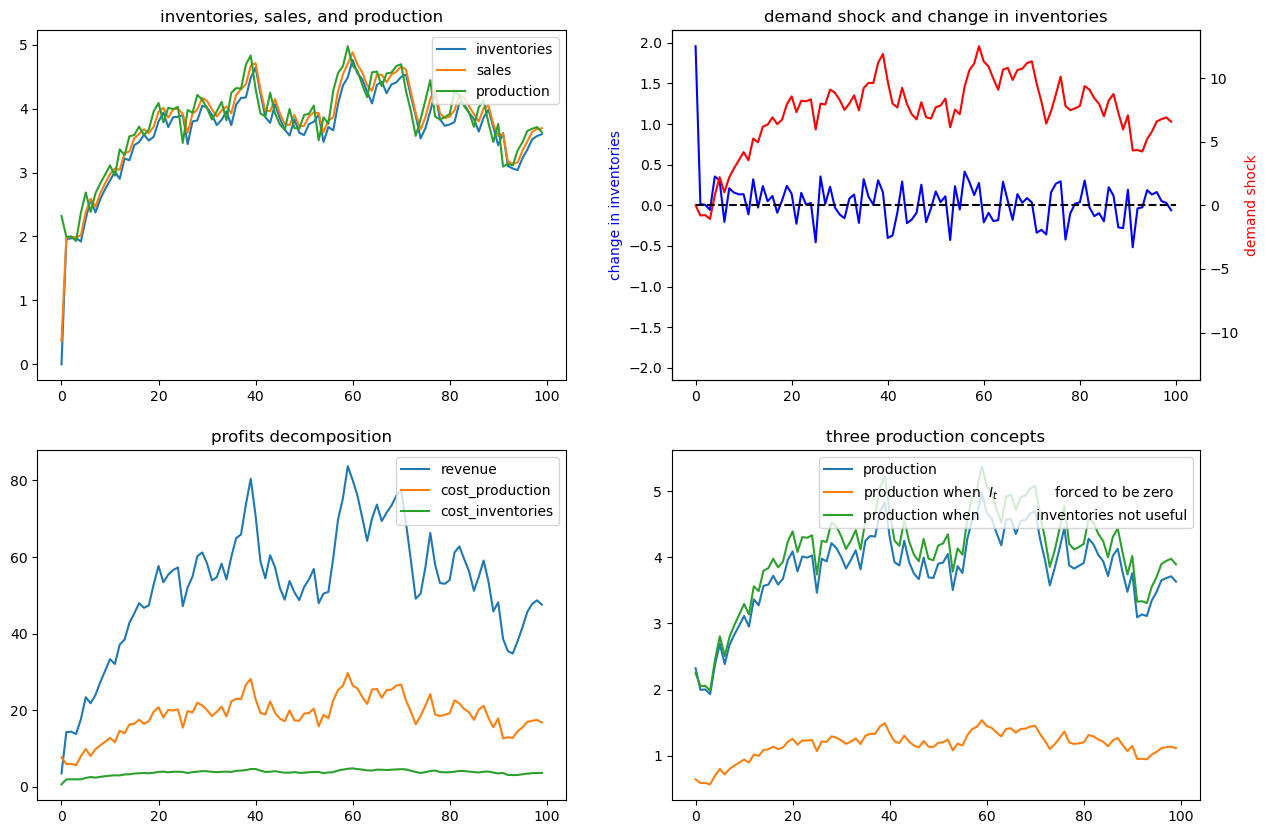

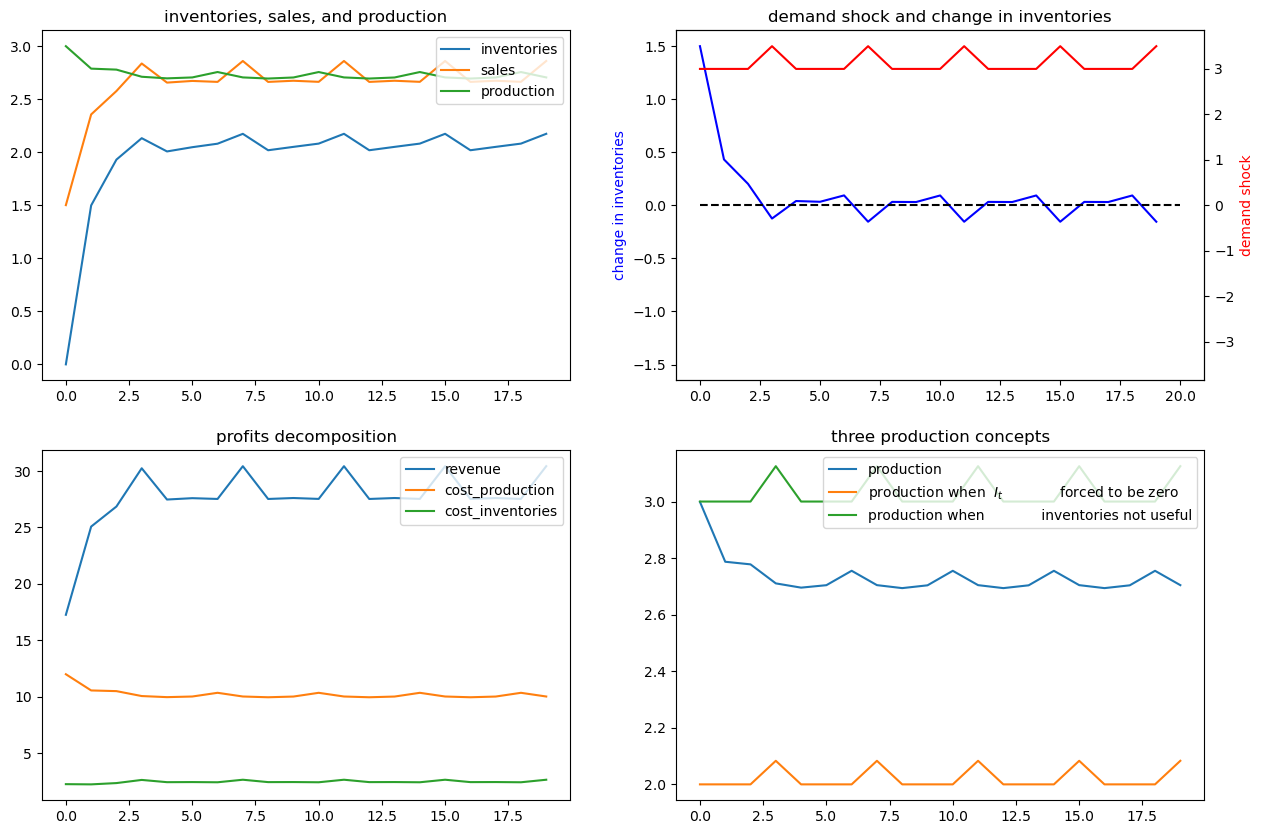

9.2. Example 1#

In this example, the demand shock follows AR(1) process:

which implies

We set \(\alpha=1\) and \(\rho=0.9\), their default values.

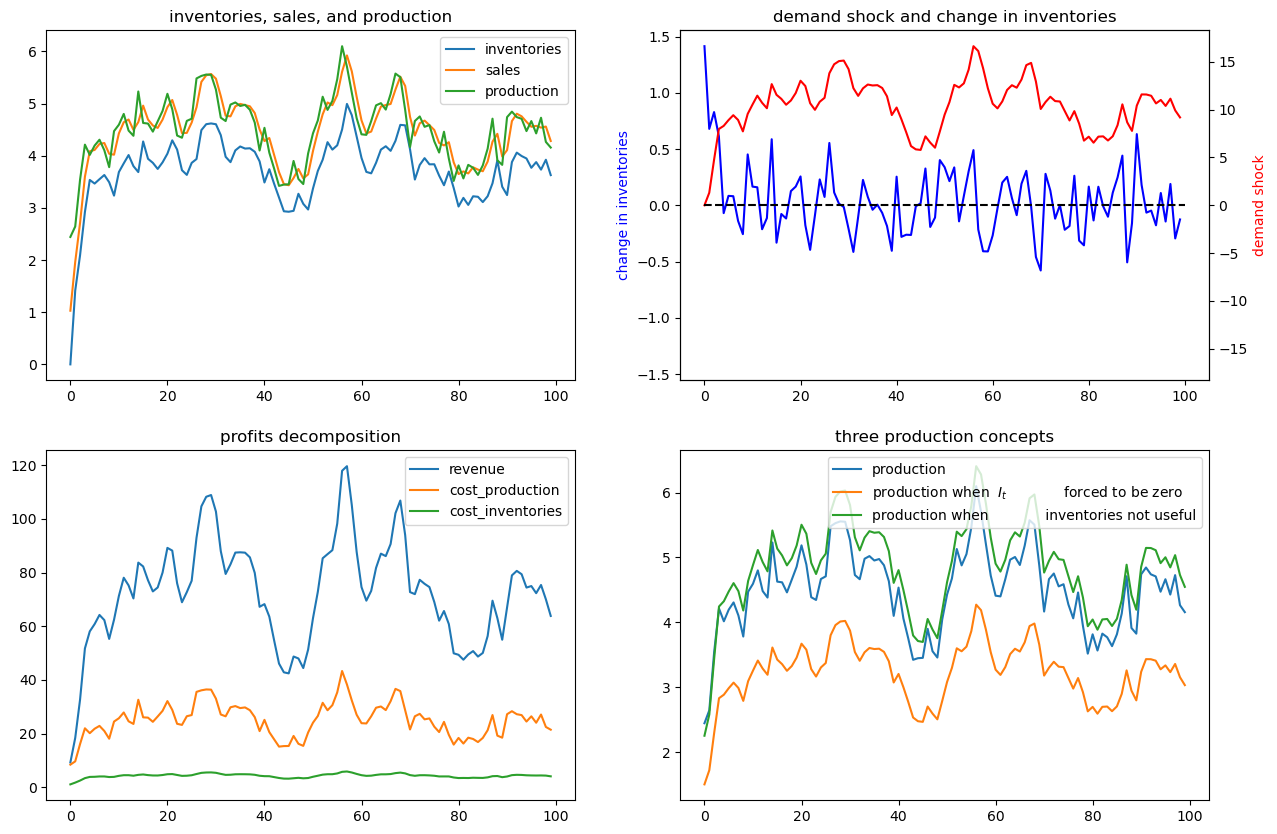

We’ll calculate and display outcomes, then discuss them below the pertinent figures.

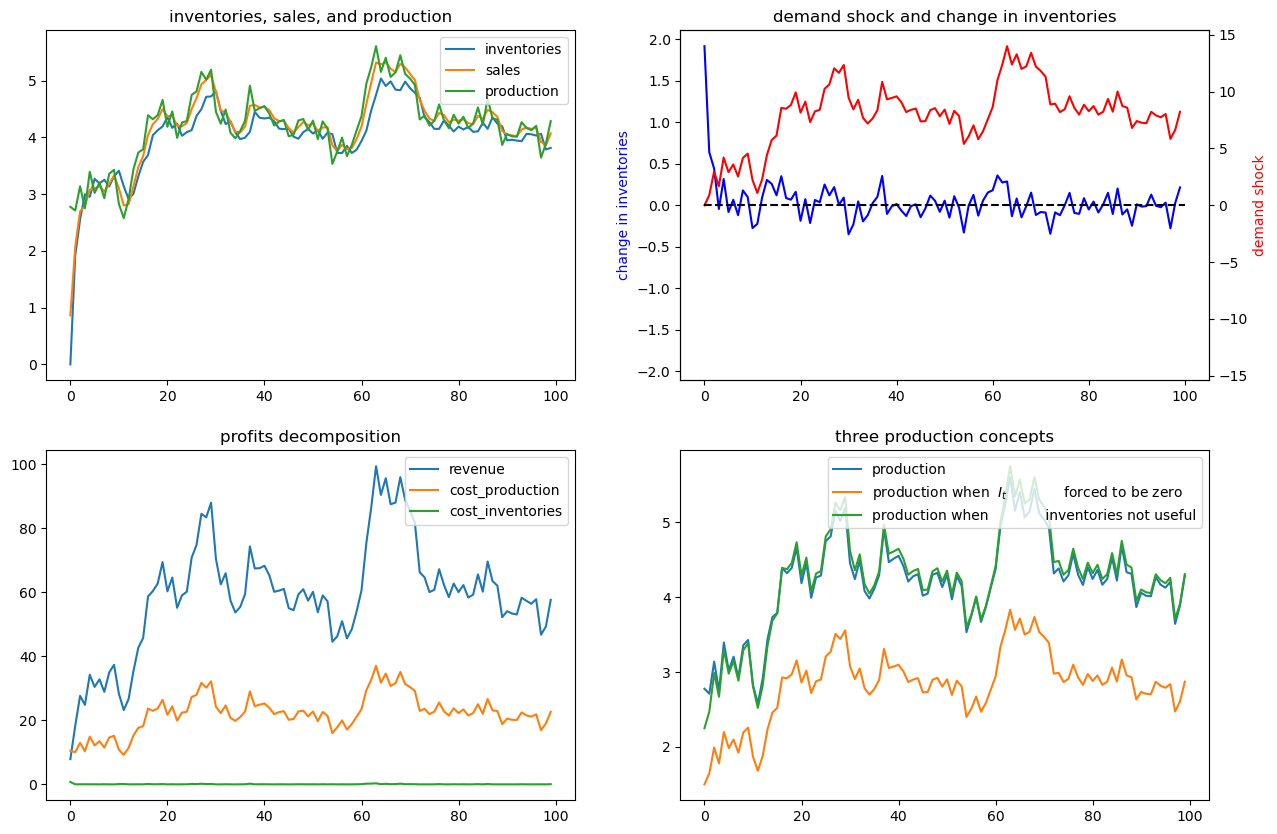

ex1 = SmoothingExample()

x0 = [0, 1, 0]

ex1.simulate(x0)

The figures above illustrate various features of an optimal production plan.

Starting from zero inventories, the firm builds up a stock of inventories and uses them to smooth costly production in the face of demand shocks.

Optimal decisions evidently respond to demand shocks.

Inventories are always less than sales, so some sales come from current production, a consequence of the cost, \(d_1 I_t\) of holding inventories.

The lower right panel shows differences between optimal production and two alternative production concepts that come from altering the firm’s cost structure – i.e., its technology.

These two concepts correspond to these distinct altered firm problems.

a setting in which inventories are not needed

a setting in which they are needed but we arbitrarily prevent the firm from holding inventories by forcing it to set \(I_t=0\) always

We use these two alternative production concepts in order to shed light on the baseline model.

9.3. Inventories Not Useful#

Let’s turn first to the setting in which inventories aren’t needed.

In this problem, the firm forms an output plan that maximizes the expected value of

It turns out that the optimal plan for \(Q_t\) for this problem also solves a sequence of static problems \(\max_{Q_t}\{p_t Q_t - c(Q_t)\}\).

When inventories aren’t required or used, sales always equal production.

This simplifies the problem and the optimal no-inventory production maximizes the expected value of

The optimum decision rule is

9.4. Inventories Useful but are Hardwired to be Zero Always#

Next, we turn to a distinct problem in which inventories are useful – meaning that there are costs of \(d_2 (I_t - S_t)^2\) associated with having sales not equal to inventories – but we arbitrarily impose on the firm the costly restriction that it never hold inventories.

Here the firm’s maximization problem is

subject to the restrictions that \(I_{t}=0\) for all \(t\) and that \(I_{t+1}=I_{t}+Q_{t}-S_{t}\).

The restriction that \(I_t = 0\) implies that \(Q_{t}=S_{t}\) and that the maximization problem reduces to

Here the optimal production plan is

We introduce this \(I_t\) is hardwired to zero specification in order to shed light on the role that inventories play by comparing outcomes with those under our two other versions of the problem.

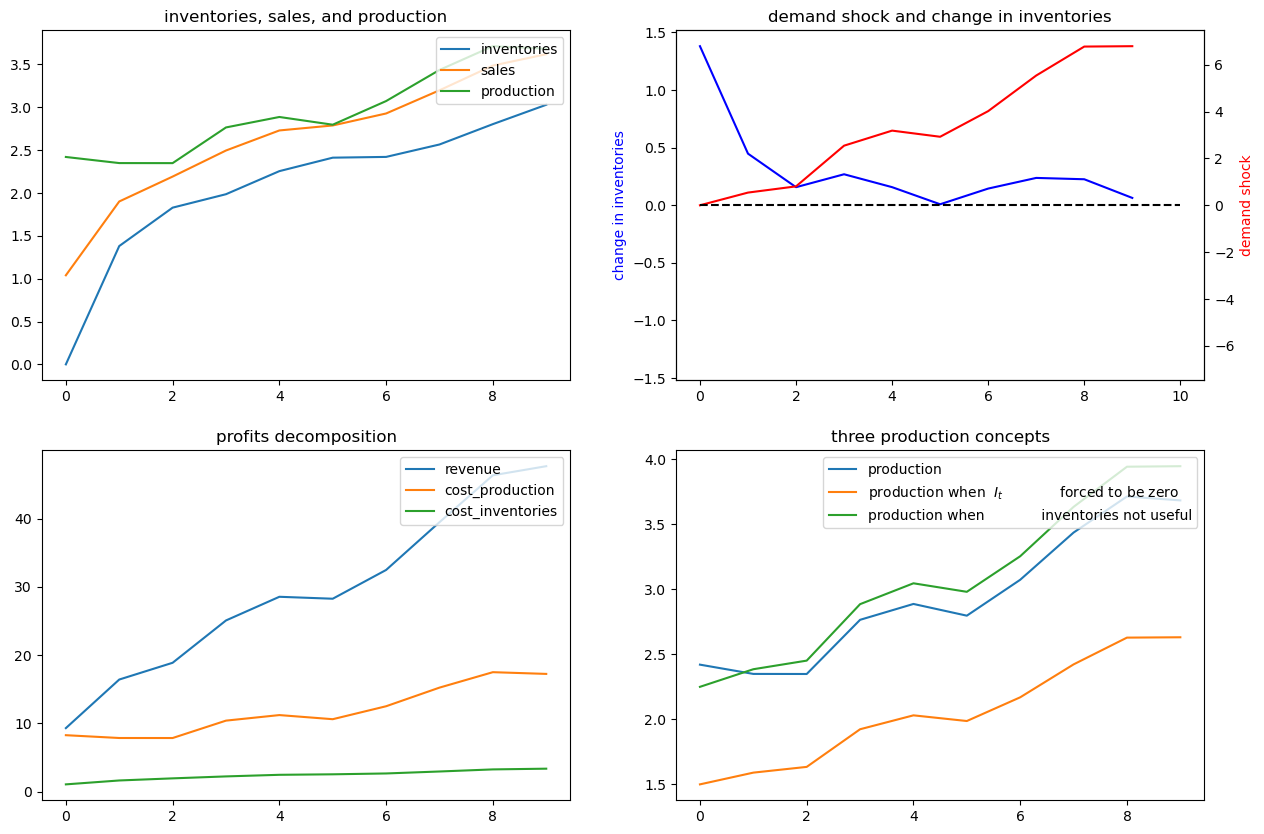

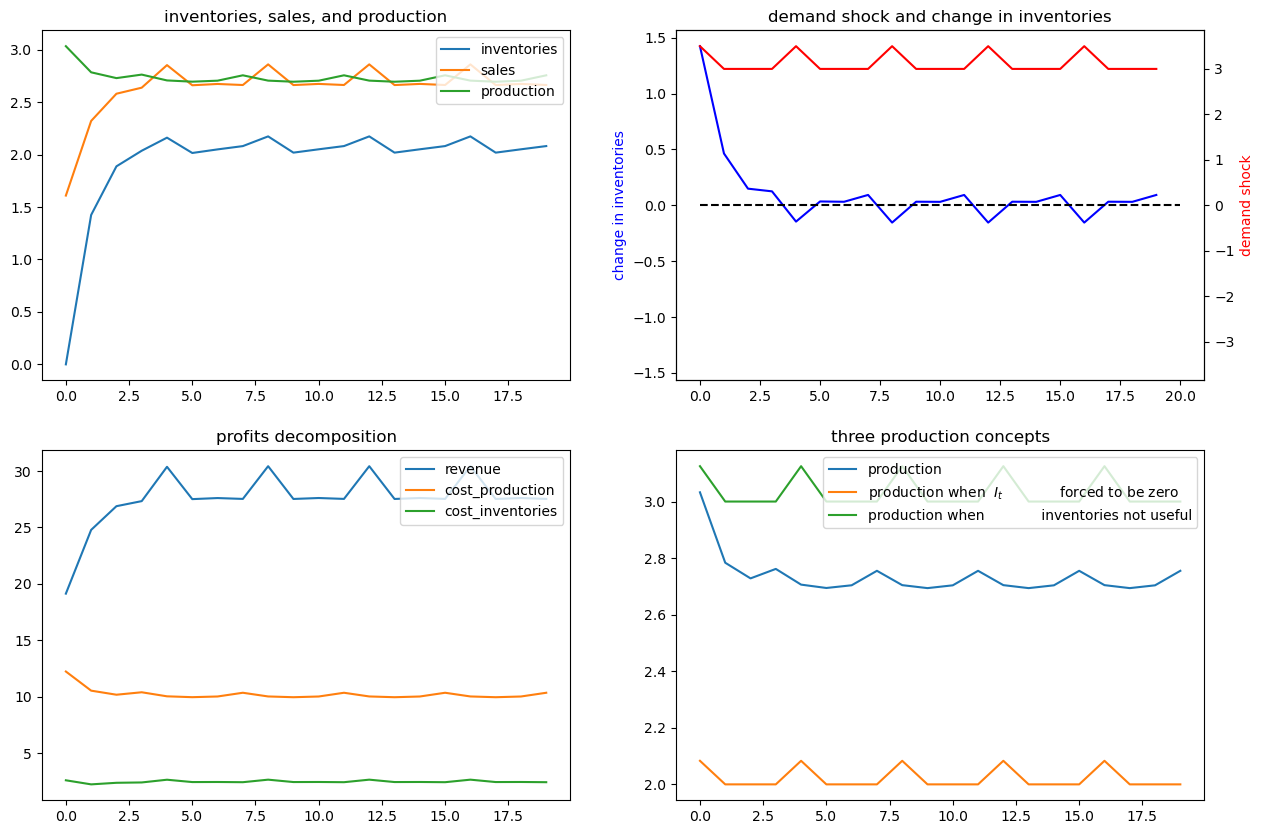

The bottom right panel displays a production path for the original problem that we are interested in (the blue line) as well with an optimal production path for the model in which inventories are not useful (the green path) and also for the model in which, although inventories are useful, they are hardwired to zero and the firm pays cost \(d(0, Q_t)\) for not setting sales \(S_t = Q_t\) equal to zero (the orange line).

Notice that it is typically optimal for the firm to produce more when inventories aren’t useful. Here there is no requirement to sell out of inventories and no costs from having sales deviate from inventories.

But “typical” does not mean “always”.

Thus, if we look closely, we notice that for small \(t\), the green “production when inventories aren’t useful” line in the lower right panel is below optimal production in the original model.

High optimal production in the original model early on occurs because the firm wants to accumulate inventories quickly in order to acquire high inventories for use in later periods.

But how the green line compares to the blue line early on depends on the evolution of the demand shock, as we will see in a deterministically seasonal demand shock example to be analyzed below.

In that example, the original firm optimally accumulates inventories slowly because the next positive demand shock is in the distant future.

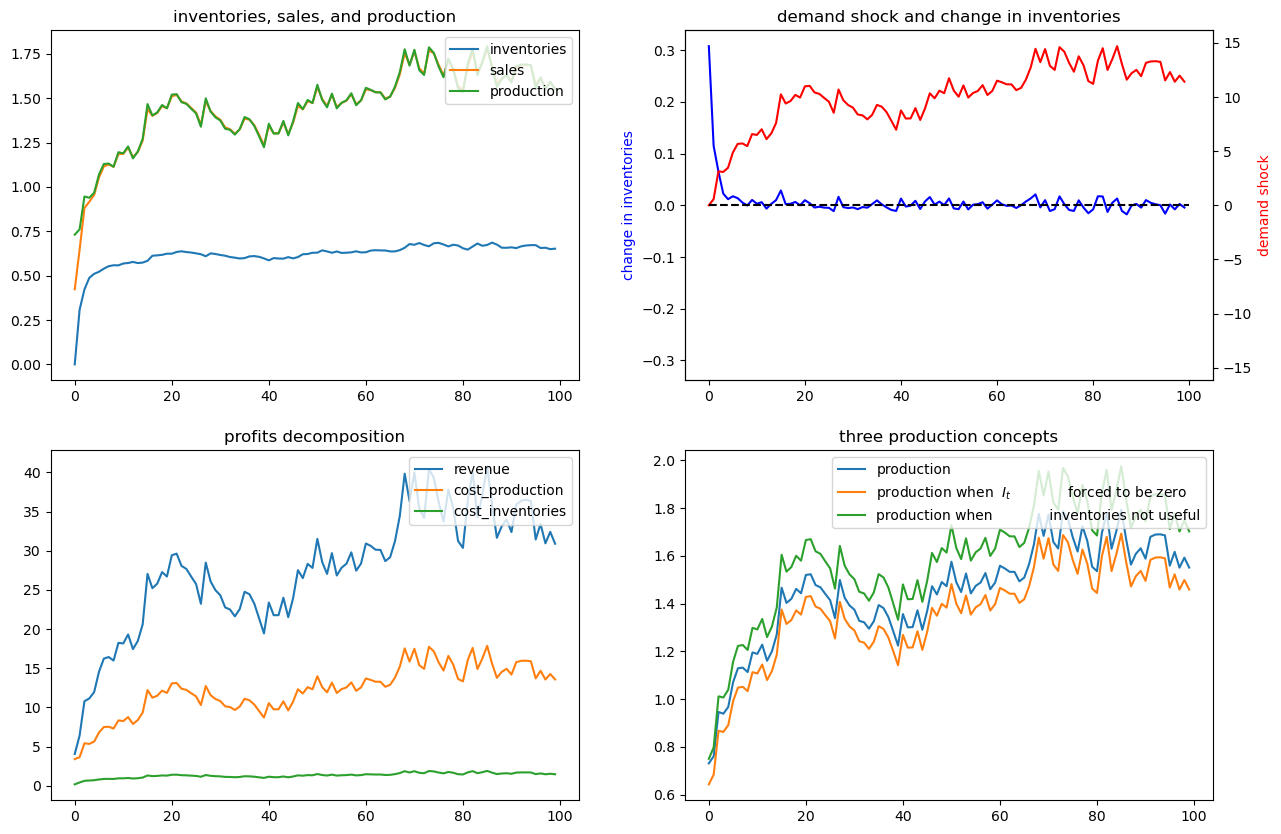

To make the green-blue model production comparison easier to see, let’s confine the graphs to the first 10 periods:

ex1.simulate(x0, T=10)

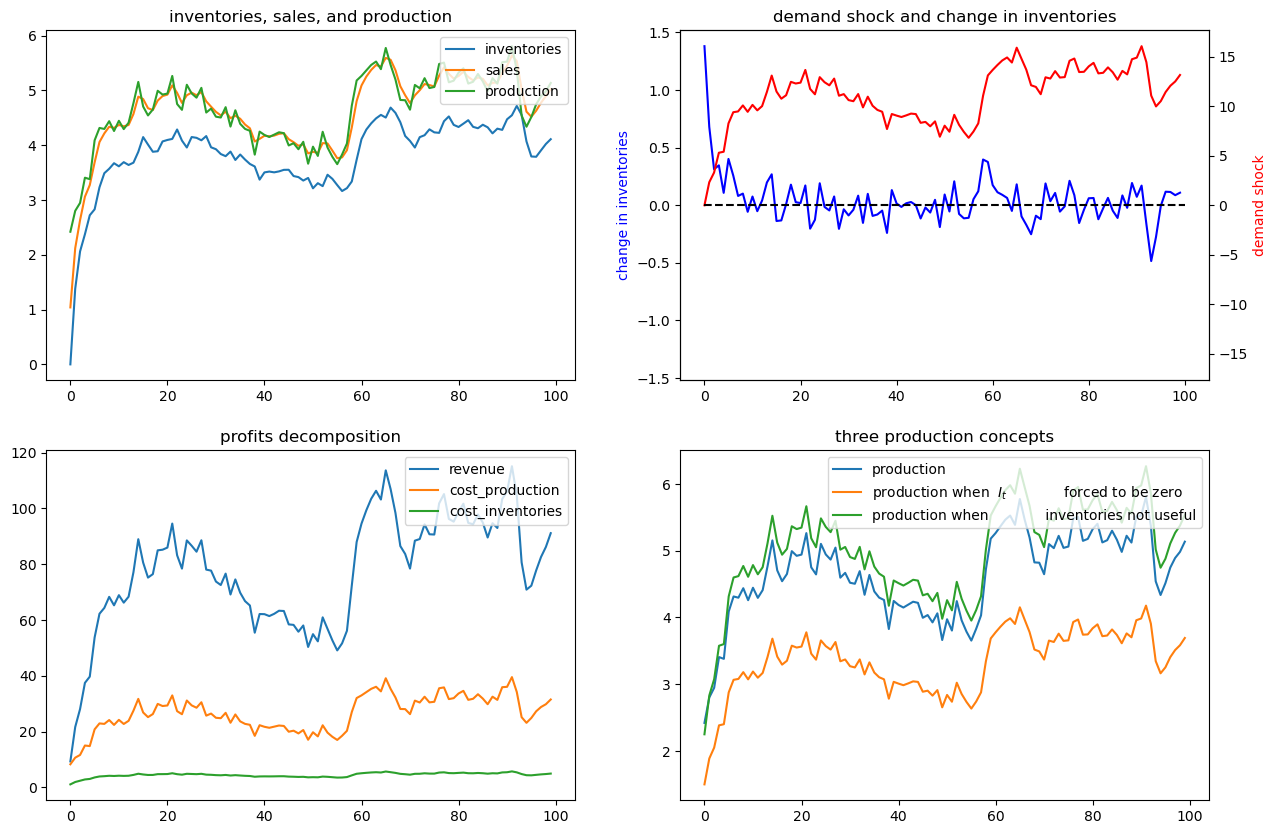

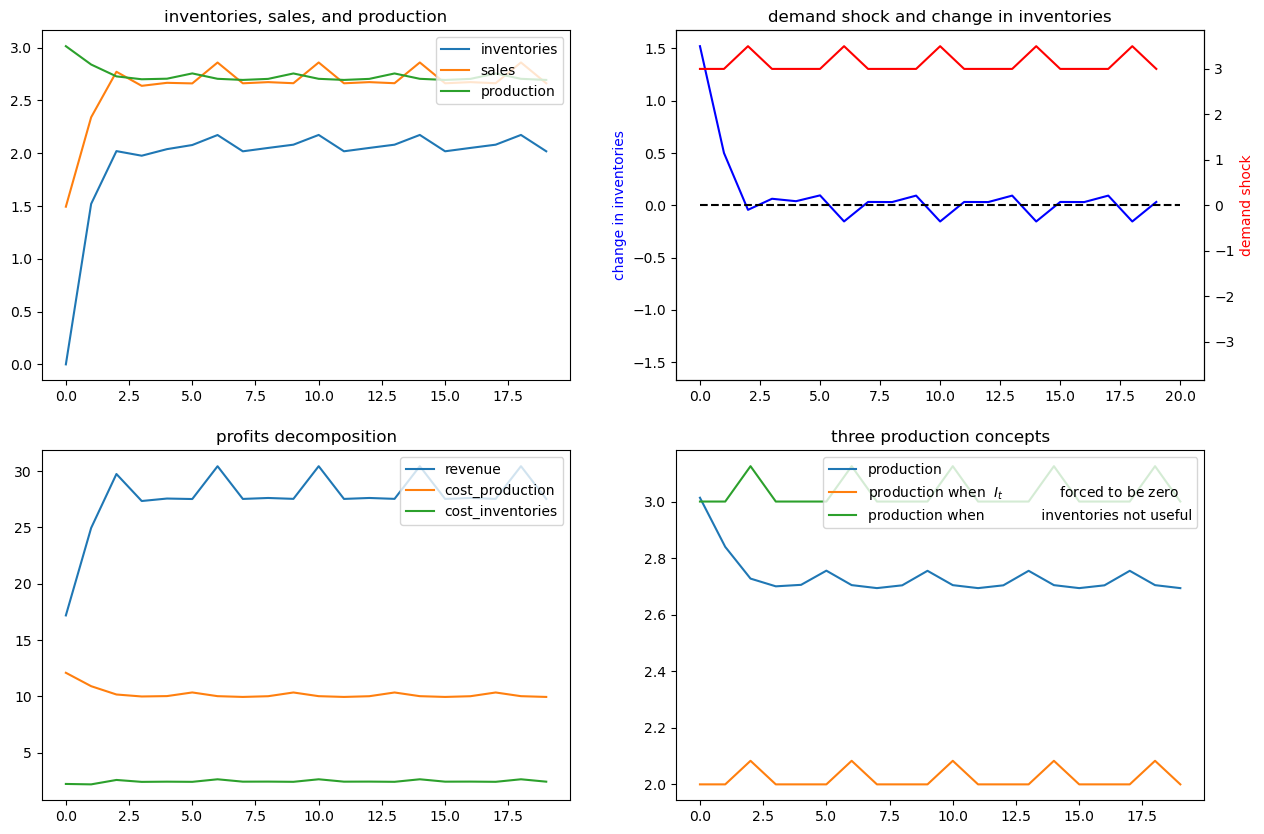

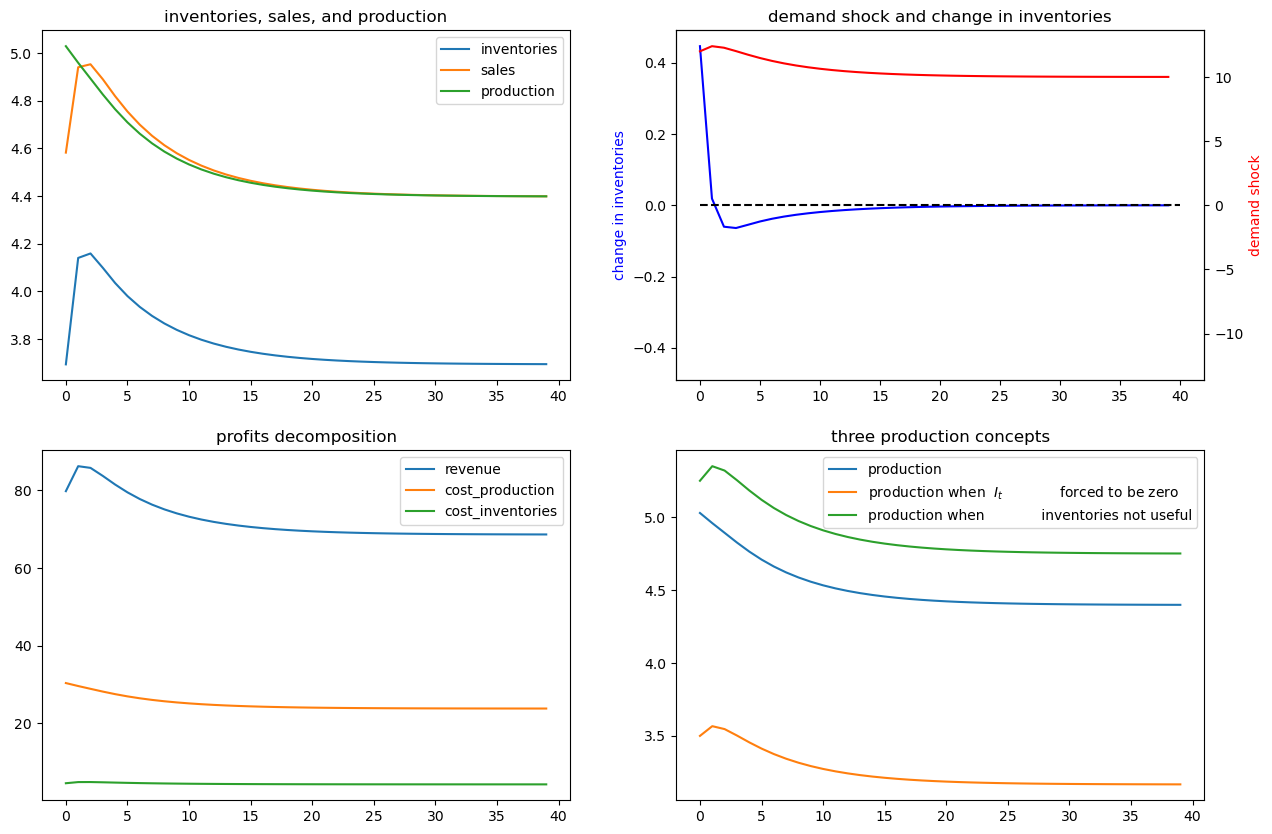

9.5. Example 2#

Next, we shut down randomness in demand and assume that the demand shock \(\nu_t\) follows a deterministic path:

Again, we’ll compute and display outcomes in some figures

ex2 = SmoothingExample(C2=[[0], [0]])

x0 = [0, 1, 0]

ex2.simulate(x0)

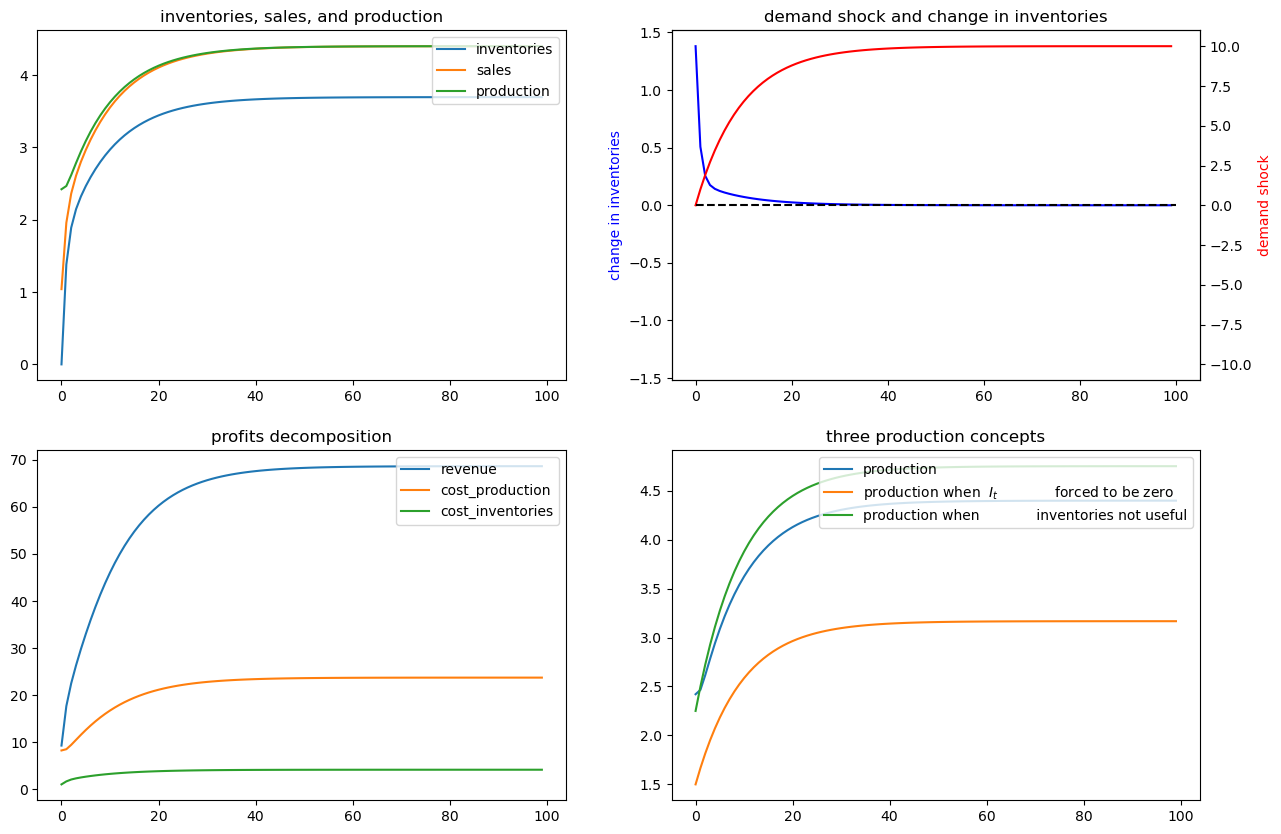

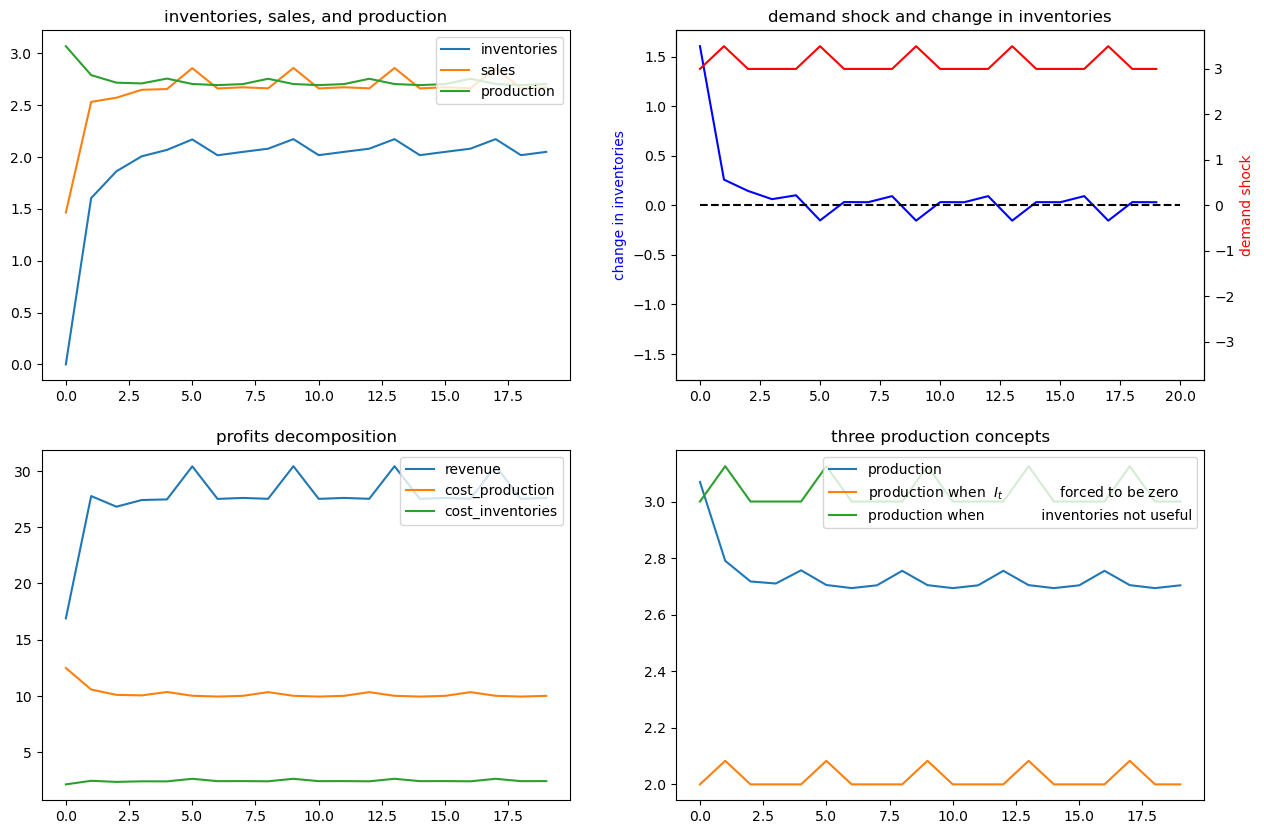

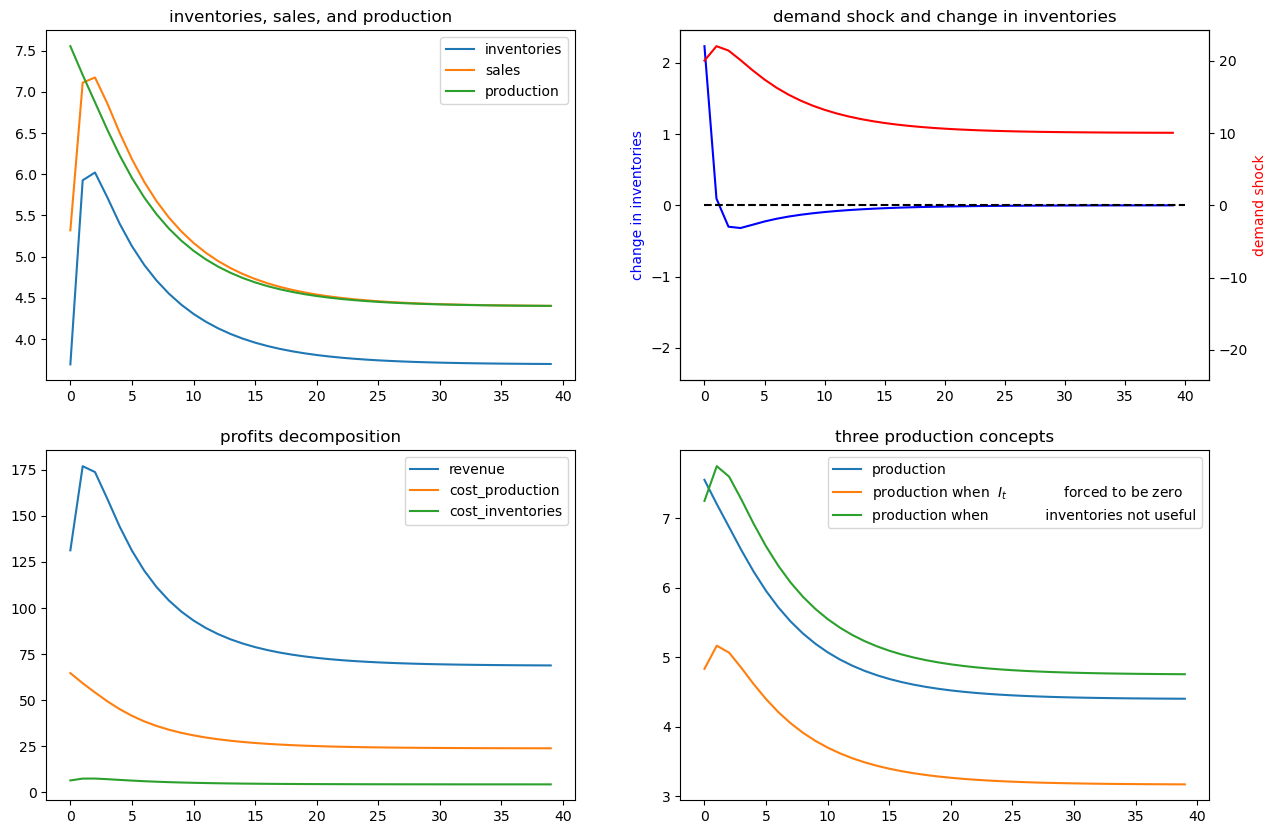

9.6. Example 3#

Now we’ll put randomness back into the demand shock process and also assume that there are zero costs of holding inventories.

In particular, we’ll look at a situation in which \(d_1=0\) but \(d_2>0\).

Now it becomes optimal to set sales approximately equal to inventories and to use inventories to smooth production quite well, as the following figures confirm

ex3 = SmoothingExample(d1=0)

x0 = [0, 1, 0]

ex3.simulate(x0)

9.7. Example 4#

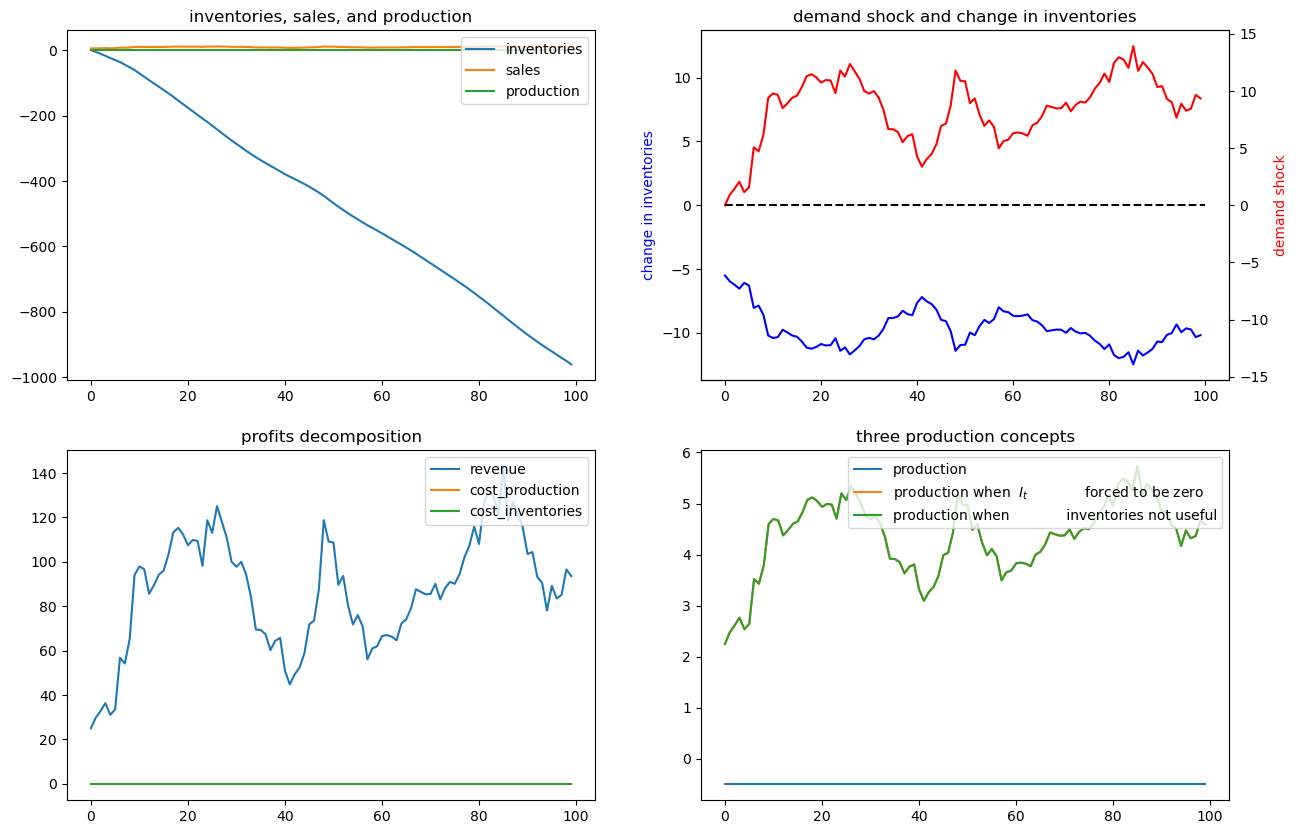

To bring out some features of the optimal policy that are related to some technical issues in linear control theory, we’ll now temporarily assume that it is costless to hold inventories.

When we completely shut down the cost of holding inventories by setting \(d_1=0\) and \(d_2=0\), something absurd happens (because the Bellman equation is opportunistic and very smart).

(Technically, we have set parameters that end up violating conditions needed to assure stability of the optimally controlled state.)

The firm finds it optimal to set \(Q_t \equiv Q^* = \frac{-c_1}{2c_2}\), an output level that sets the costs of production to zero (when \(c_1 >0\), as it is with our default settings, then it is optimal to set production negative, whatever that means!).

Recall the law of motion for inventories

So when \(d_1=d_2= 0\) so that the firm finds it optimal to set \(Q_t = \frac{-c_1}{2c_2}\) for all \(t\), then

for almost all values of \(S_t\) under our default parameters that keep demand positive almost all of the time.

The dynamic program instructs the firm to set production costs to zero and to run a Ponzi scheme by running inventories down forever.

(We can interpret this as the firm somehow going short in or borrowing inventories)

The following figures confirm that inventories head south without limit

ex4 = SmoothingExample(d1=0, d2=0)

x0 = [0, 1, 0]

ex4.simulate(x0)

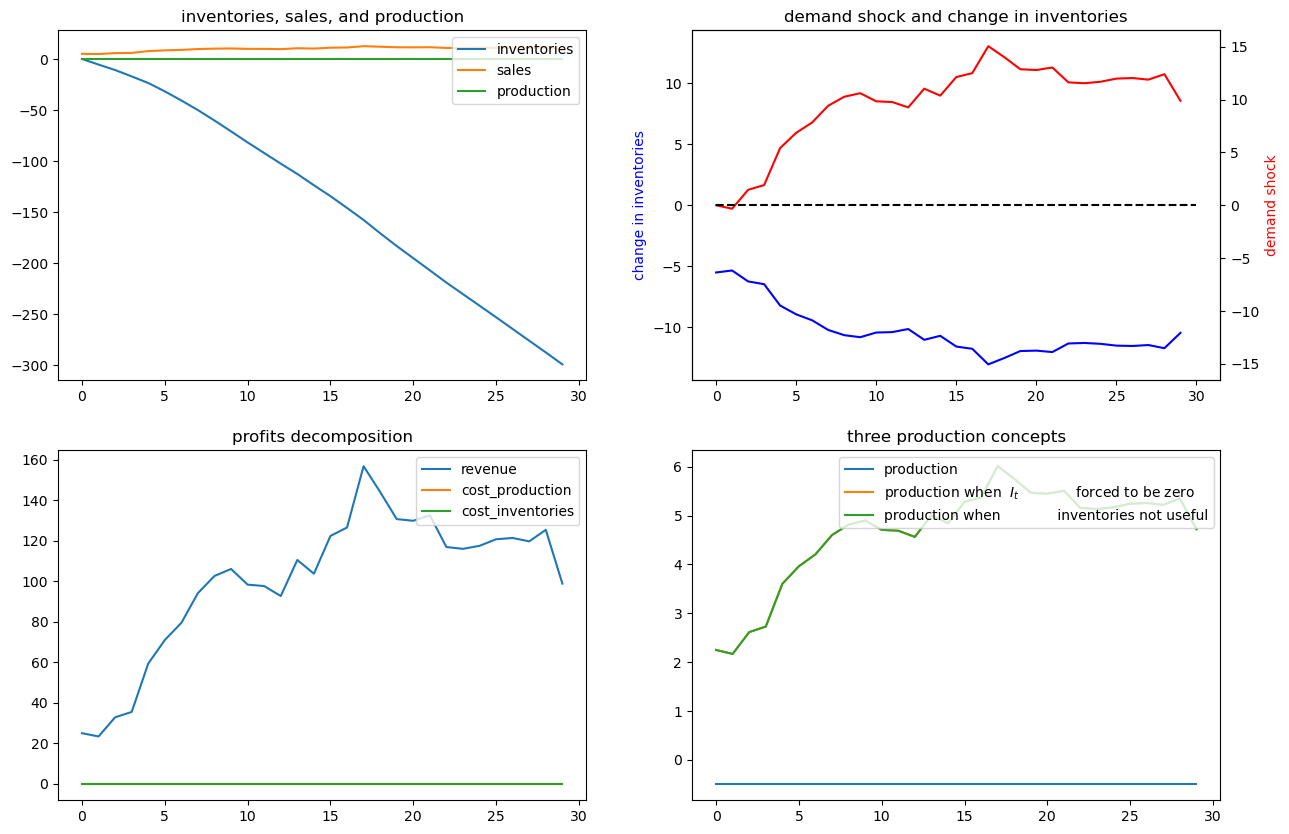

Let’s shorten the time span displayed in order to highlight what is going on.

We’ll set the horizon \(T =30\) with the following code

# shorter period

ex4.simulate(x0, T=30)

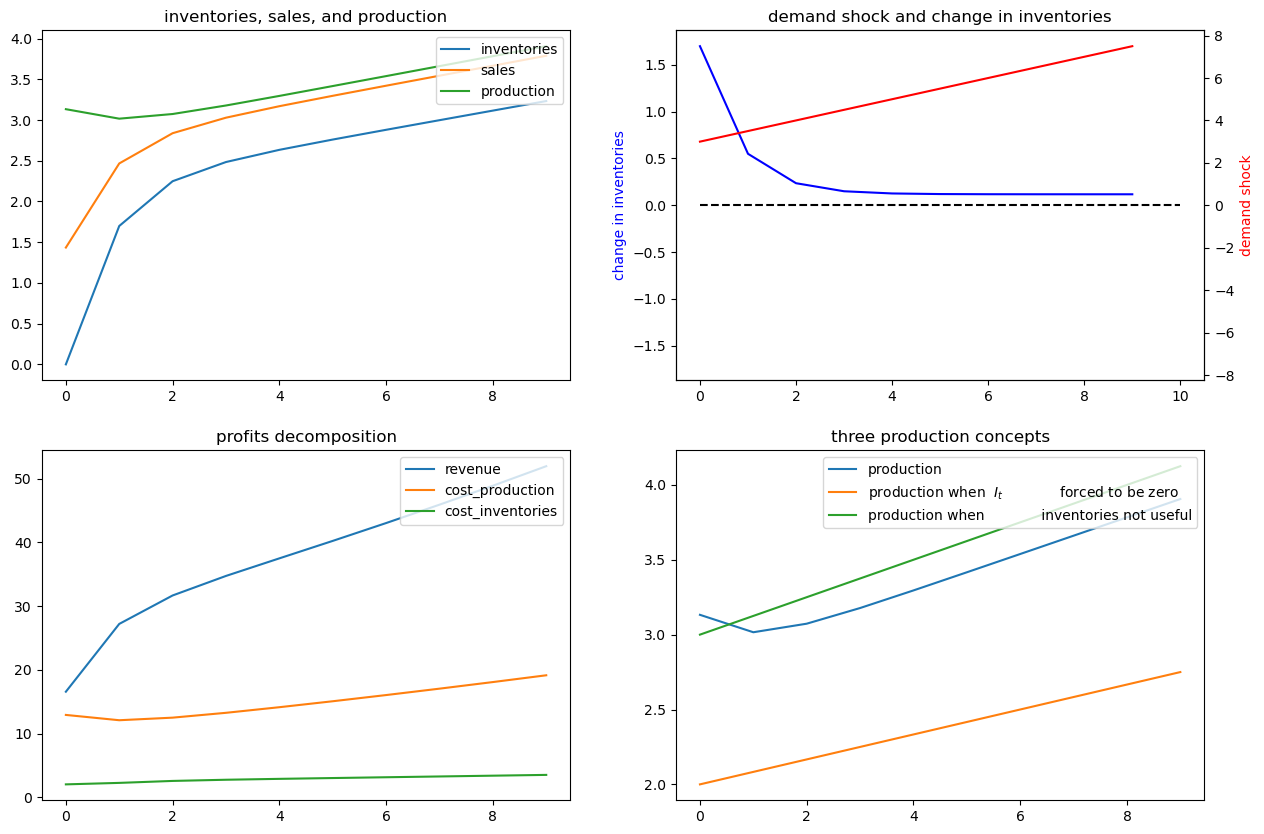

9.8. Example 5#

Now we’ll assume that the demand shock that follows a linear time trend

To represent this, we set \(C_2 = \begin{bmatrix} 0 \cr 0 \end{bmatrix}\) and

# Set parameters

a = 0.5

b = 3.

ex5 = SmoothingExample(A22=[[1, 0], [1, 1]], C2=[[0], [0]], G=[b, a])

x0 = [0, 1, 0] # set the initial inventory as 0

ex5.simulate(x0, T=10)

9.9. Example 6#

Now we’ll assume a deterministically seasonal demand shock.

To represent this we’ll set

where \(a > 0, b>0\) and

ex6 = SmoothingExample(A22=[[1, 0, 0, 0, 0],

[0, 0, 0, 0, 1],

[0, 1, 0, 0, 0],

[0, 0, 1, 0, 0],

[0, 0, 0, 1, 0]],

C2=[[0], [0], [0], [0], [0]],

G=[b, a, 0, 0, 0])

x00 = [0, 1, 0, 1, 0, 0] # Set the initial inventory as 0

ex6.simulate(x00, T=20)

Now we’ll generate some more examples that differ simply from the initial season of the year in which we begin the demand shock

x01 = [0, 1, 1, 0, 0, 0]

ex6.simulate(x01, T=20)

x02 = [0, 1, 0, 0, 1, 0]

ex6.simulate(x02, T=20)

x03 = [0, 1, 0, 0, 0, 1]

ex6.simulate(x03, T=20)

9.10. Exercises#

Please try to analyze some inventory sales smoothing problems using the

SmoothingExample class.

Exercise 9.1

Assume that the demand shock follows AR(2) process below:

where \(\alpha=1\), \(\rho_{1}=1.2\), and \(\rho_{2}=-0.3\).

You need to construct \(A22\), \(C\), and \(G\) matrices

properly and then to input them as the keyword arguments of

SmoothingExample class. Simulate paths starting from the initial

condition \(x_0 = \left[0, 1, 0, 0\right]^\prime\).

After this, try to construct a very similar SmoothingExample with

the same demand shock process but exclude the randomness

\(\epsilon_t\). Compute the stationary states \(\bar{x}\) by

simulating for a long period. Then try to add shocks with different

magnitude to \(\bar{\nu}_t\) and simulate paths. You should see how

firms respond differently by staring at the production plans.

Solution to Exercise 9.1

# set parameters

α = 1

ρ1 = 1.2

ρ2 = -.3

# construct matrices

A22 =[[1, 0, 0],

[1, ρ1, ρ2],

[0, 1, 0]]

C2 = [[0], [1], [0]]

G = [0, 1, 0]

ex1 = SmoothingExample(A22=A22, C2=C2, G=G)

x0 = [0, 1, 0, 0] # initial condition

ex1.simulate(x0)

# now silence the noise

ex1_no_noise = SmoothingExample(A22=A22, C2=[[0], [0], [0]], G=G)

# initial condition

x0 = [0, 1, 0, 0]

# compute stationary states

x_bar = ex1_no_noise.LQ.compute_sequence(x0, ts_length=250)[0][:, -1]

x_bar

array([ 3.69387755, 1. , 10. , 10. ])

In the following, we add small and large shocks to \(\bar{\nu}_t\) and compare how firm responds differently in quantity. As the shock is not very persistent under the parameterization we are using, we focus on a short period response.

T = 40

# small shock

x_bar1 = x_bar.copy()

x_bar1[2] += 2

ex1_no_noise.simulate(x_bar1, T=T)

# large shock

x_bar1 = x_bar.copy()

x_bar1[2] += 10

ex1_no_noise.simulate(x_bar1, T=T)

Exercise 9.2

Change parameters of \(C(Q_t)\) and \(d(I_t, S_t)\).

Make production more costly, by setting \(c_2=5\).

Increase the cost of having inventories deviate from sales, by setting \(d_2=5\).

Solution to Exercise 9.2

x0 = [0, 1, 0]

SmoothingExample(c2=5).simulate(x0)

SmoothingExample(d2=5).simulate(x0)